Navan: The Travel Company That Refused to Die (From COVID Zero to IPO)

Next upcoming IPO is Navan (formerly TripActions), an all-in-one corporate travel and expense management platform headquartered in Palo Alto, California. It offers a fully integrated solution for businesses, combining travel booking, corporate-issued payment cards, automated expense reporting, and analytics.

Let’s take a look to see how the potential returns look for investors and employees. Please note that we will be using the estimated opening day IPO price of $25 for this analysis, based on the range given by news reports. Most employees/investors will have a 6-month lockup period, so their actual returns may vary depending on how the market views the company. These are certainly only preliminary numbers, as we’ve learned from Circle, Coreweave and Figma, a lot can happen in the lockup period.

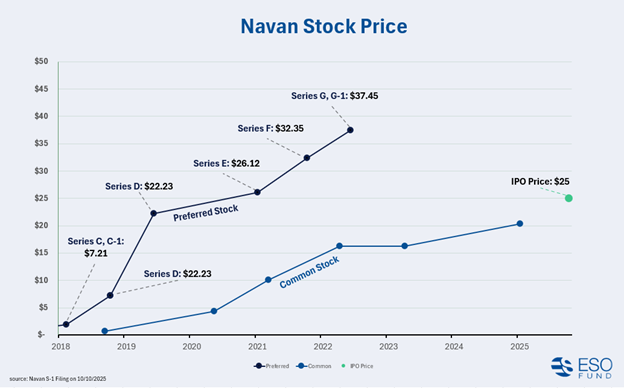

Below is a graph of Navan’s preferred and common stock pricing over time taken from the S1 they filed. Please note that we only include rounds and data point priced from 2018 onwards.

Series Seed (101.26x, Apr 2015), Series A (50.02x, Feb 2016), Series A-1 (42.71x, Apr 2017), Series B (13.40x, Feb 2018) no surprise, all these early investors did amazing. If you invest early you have higher risk, but also higher returns. Even the Series B investors smoked the S&P which had a 2.49x return simultaneously.

Series C, C-1 (3.47x, Oct 2018), Very solid returns for these investors and I’m sure they’re pretty happy about it. They’re handedly beating the S&P which had a 2.59x within that time.

Series D (1.12x), not the best returns here, these investors are barely getting their money back after a 5-year hold period and got beaten by the S&P, which had a 2.36x return.

Series E (0.96x), Series F (0.77x),Series G, G-1 (0.67x), all these later stage investors are losing money, it’s a tough one here. All these investors are regretting this one, they lost to the S&P by a wide margin as well, which had returned more than 1.5x compared to the Series, E, F, G & G-1.

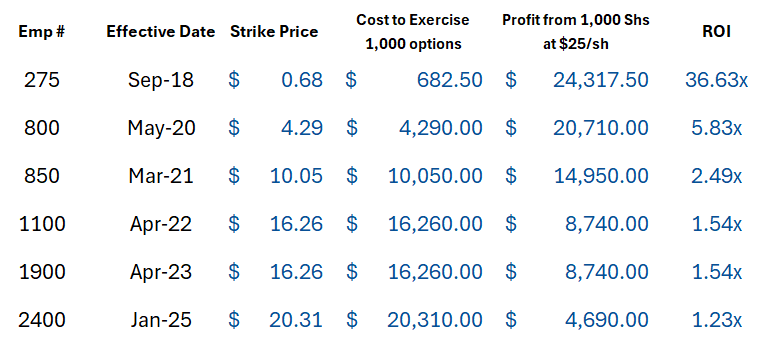

Employees time! Below are the strike prices (the price employees pay to exercise their options) we could find at certain dates according to the S1. We also put the company size (Emp #) at each strike price date so you can get a feel for how many people were getting each strike price. This also includes the cost to exercise 1,000 shares, and what those shares are worth today. All exercise costs assume $0 in taxes, which is unfortunately rarely the case, but this allows us to compare these gross amounts apples to apples - as if they are being exercised and sold today. Typically, there will be either short or long-term capital gains associated with the sale (on top of AMT or income tax at the time of exercise). Read this page for more on stock option taxes.

The takeaway from the graph above is that most employees did solid, but not incredible. Of course, some of the earlier employees did awesome, even those who started in 2020 got a 5.83x. However, it looks like a majority of the company appears to have started within the last three years, and they are getting a 1.54x at best, which is not a terrible return. But if you’re an employee at a startup company you are probably hoping for a little better than that.

Another interesting note here is that many employees had a repricing of their grants. Originally the grant prices in 2022 were priced at $20.73, but the company ended up repricing them to $16.26. This type of repricing typically only happens to common stock and is a good tool under the company’s belt they can use to incentive and boost employee morale. This type of repricing is very employee friendly, and not something the company is required to do.

Written by Sam Stroud, Investor at ESO Fund

Yes, all the data points that we recieved from the S1 had employees making money.

Most employees must wait 6 months after the IPO to sell due to a lockup period.

Yes, ESO Fund does offer IPO Lockup Loans to cover the cost of exercise during your lockup period.

Equity decisions are complex, but you don’t have to navigate them alone. ESO Fund has been helping employees unlock the value of their hard-earned equity for over a decade. Whether you’re exercising, planning for taxes, or looking for liquidity, we’re here to provide clear, non-recourse funding solutions tailored to your situation.

📘 Overview of How We Work

See our 3-step process.

⏰ Option Exercise Funding

Exercise without risking savings.

⭐ Client Reviews

Hear from employees we’ve helped succeed.

🚀 Share Liquidity

Unlock cash while keeping your shares.

📊 AMT Calculator

Estimate tax exposure in minutes.

🤝 RSU Liquidity

Access liquidity from vested RSUs before IPO.

Ready to explore your equity options? Our team is here to walk you through the next steps.

Schedule a Call

This innovative service promotes and enables a healthier relationship between companies and employees. I my opinion it's valuable to employees and great for the overall tech environment and economy. It is good for nobody when employees feel trapped because they can't afford to leave. In less extreme cases exercising can be expensive and somewhat risky and this is simply a good smart hedge and a good square deal. Brilliant!